They Do Not Know What's Coming

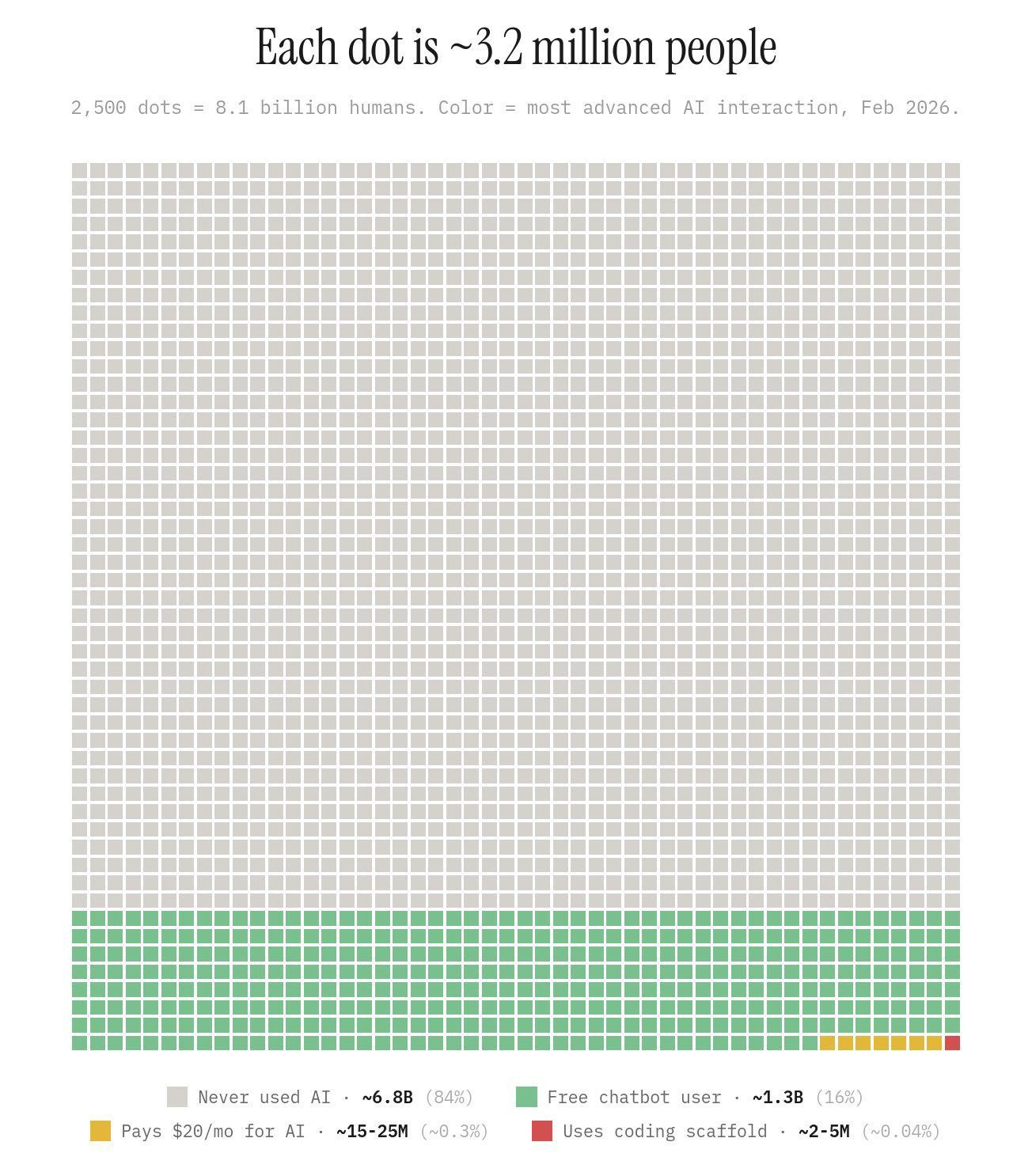

Generative AI is transforming work, and 85% of the connected world hasn't tried it once.

If you’re like me, you saw this graphic above at least 10 times over the past few days.

Of course it makes sense that large swaths of the global population do not and indeed cannot access AI models — over 2 billion people globally still live entirely without internet. And in many regions with internet access, the infrastructure is insufficient to support AI usage. Even in high-income countries, only one quarter of the population uses AI according to the World Bank. This in itself is not particularly interesting.

But if you’re, like me, an avid user of frontier AI models, you saw the graphic and probably thought:

Very few people have even the slightest clue of what’s happening… and what’s still to come.

I'll have more to say about the implications of this in a project I'm working on. For now, I wanted to share the current state of AI adoption to contribute some background research to the discussion of just how early we are in the adoption curve of this transformative technology.

This report, of course, was assembled with the help of my trusted companions Claude, ChatGPT, and the new Gemini 3.1 model. All of us may be wrong. But the direction isn’t.

Executive Summary

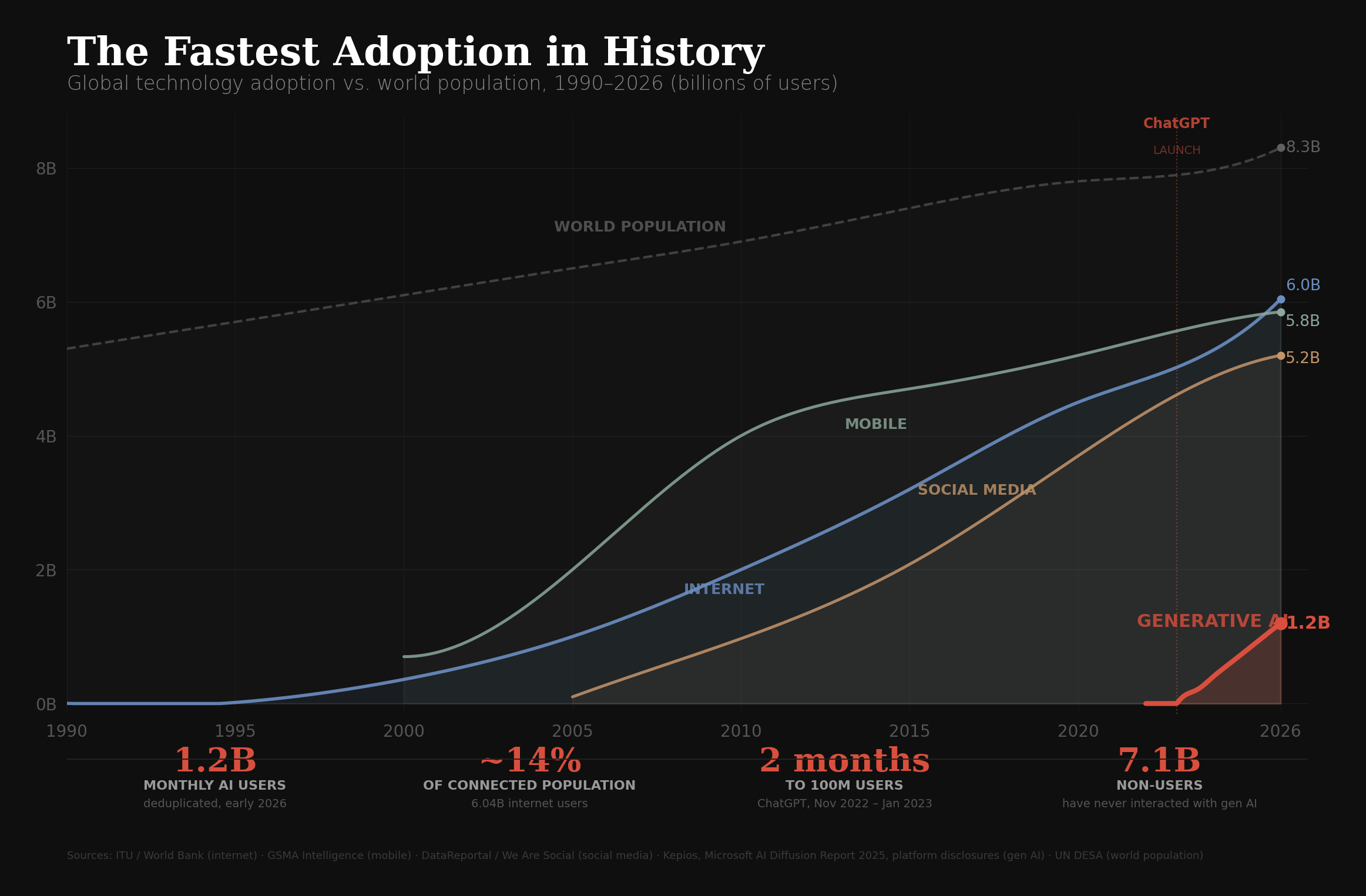

As of the first quarter of 2026, the global integration of generative artificial intelligence has unequivocally transitioned from an era of early-adopter experimentation to an era of mainstream, infrastructural utility. Driven by the aggressive proliferation of large language models, deeply embedded virtual assistants, and advanced multimodal generation tools, human interaction with generative artificial intelligence has achieved an unprecedented scale and velocity of adoption. Synthesizing data from supranational institutions, corporate financial disclosures, and independent analytics firms, the current analysis estimates that approximately 1.2 billion unique individuals globally interact with generative artificial intelligence tools on a monthly basis.

This adoption curve represents one of the fastest technological diffusions in recorded human history, fundamentally altering global digital behavior, information retrieval, and creative production. However, the surface-level metrics frequently obscure a highly fragmented landscape characterized by extensive platform overlap, stark geographic disparities, and a rapidly widening digital economic divide. While the aggregate sum of Monthly Active Users across all major consumer artificial intelligence platforms exceeds 3 billion, adjusting for the phenomenon of multi-homing—where power users simultaneously operate ChatGPT, Gemini, Claude, and Perplexity—reveals a much smaller, albeit highly engaged, unique human user base.

The enterprise and professional sectors have also demonstrated rapid, sustained monetization. Paid consumer subscriptions and enterprise software-as-a-service artificial intelligence seats currently capture an estimated 45 million paying users globally, led overwhelmingly by OpenAI’s ChatGPT Plus ecosystem and Microsoft’s Copilot integrations. In the highly technical software development domain, generative artificial intelligence has achieved near-ubiquity; approximately 80% of the world’s 28.7 million software developers currently utilize artificial intelligence coding assistants, though sustained trust in automated output remains a critical point of operational friction.

Despite these staggering figures, generative artificial intelligence remains a highly exclusive technology on a global macroeconomic scale. Out of a projected global population of 8.3 billion in 2026, an estimated 7.1 billion individuals have not interacted with generative artificial intelligence in any meaningful capacity. Even when isolating the analysis strictly to the 6.04 billion human beings with reliable internet access, nearly 80% remain non-users. This non-user population is heavily concentrated in the Global South and low-income economies, where adoption rates languish below 1%, contrasting sharply with the 24.7% adoption rate observed across the Global North.

This report provides an exhaustive, source-backed mapping of the current state of global human interaction with generative artificial intelligence. It establishes a demographic and infrastructural baseline, deconstructs platform-level usage data to separate marketing inflation from active engagement, estimates paid subscription and developer adoption rates, and rigorously evaluates the geographic, economic, and methodological constraints that define the 2026 generative artificial intelligence landscape. The objective is to produce the most defensible current estimate of total human interaction, active users, paying users, developer adoption, and the non-user population, complete with transparent uncertainty ranges.

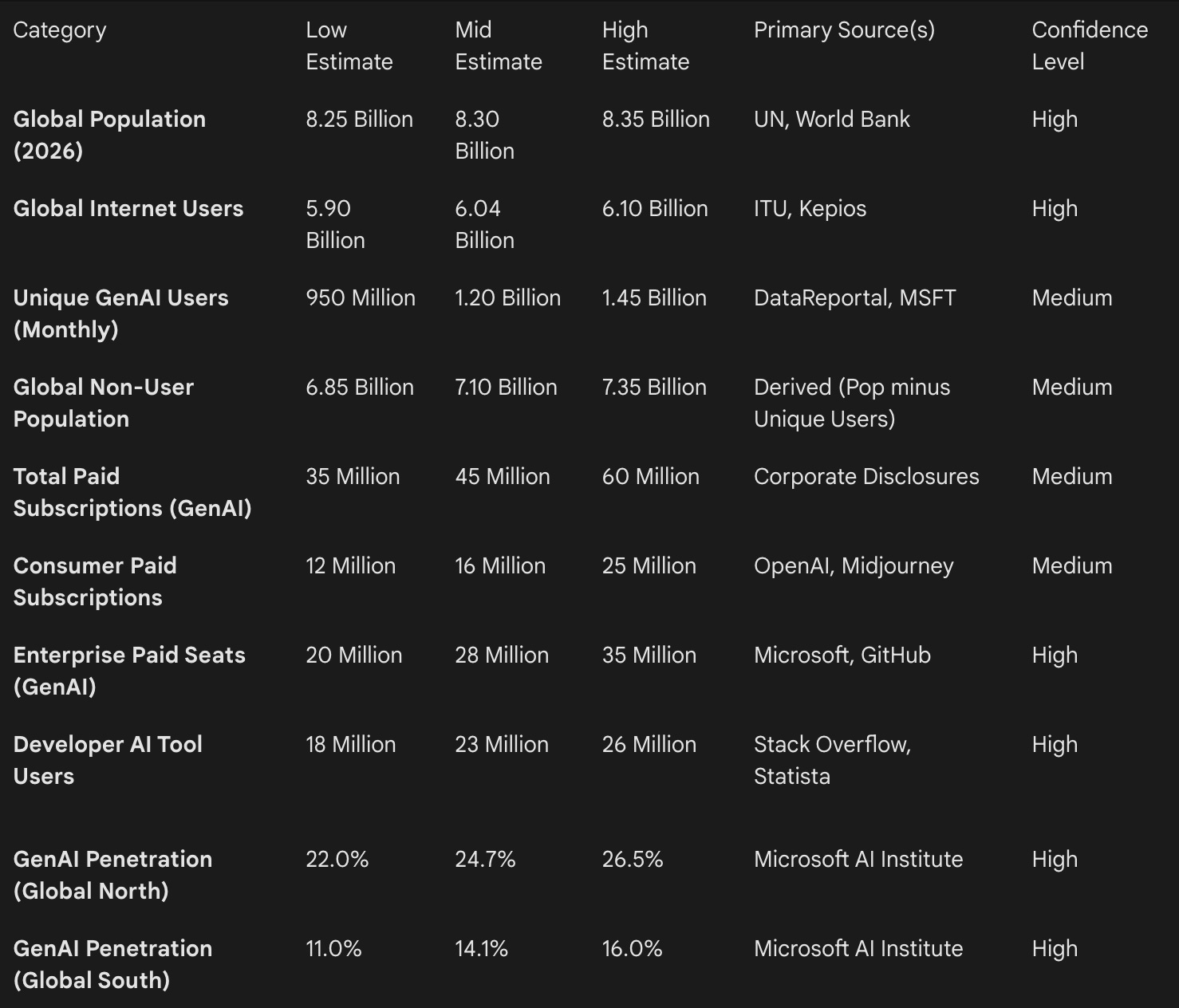

Structured Data Summary: Global Generative AI Interaction Estimates (2026)

The following table presents bounded estimates mapping the current state of human interaction with generative artificial intelligence. Estimates are categorized by low, mid, and high confidence intervals to account for opaque corporate reporting, unverified proprietary analytics, and platform overlap.

Global Baseline Context

To accurately contextualize the sheer scale and profound limitations of generative artificial intelligence adoption, it is imperative to establish the fundamental infrastructural and demographic realities of the global population as of 2026. The penetration of generative artificial intelligence is not an isolated phenomenon; it is inextricably linked to pre-existing digital infrastructure, specifically broadband internet connectivity and mobile device ownership. Without access to the underlying telecommunications framework, participation in the generative artificial intelligence ecosystem is technologically impossible.

As of 2026, the United Nations Department of Economic and Social Affairs estimates the global human population to be approximately 8.3 billion.1 This represents an increase of more than a quarter of a billion people since the global population crossed the 8 billion threshold in November 2022.1 The global median age currently stands at 31.1 years, indicating a relatively young global demographic distribution that is historically more receptive to rapid digital technology adoption.1 The distribution of this population is heavily skewed toward Asia and Africa, with India at 1.47 billion, China at 1.42 billion, and the United States at 347.8 million representing the largest individual national cohorts.2

Digital infrastructure has expanded significantly over the past half-decade, though universal access remains an unrealized ambition. According to baseline data provided by the International Telecommunication Union and independent analysis by digital insights firm Kepios, global internet penetration has reached an estimated 73.2% to 74% of the global population.3 This equates to approximately 6.04 billion individuals currently maintaining online connectivity.5 This metric represents a steady, continuous increase, with the global internet user total expanding by roughly 294 million users year-over-year, delivering a growth rate of 5.1%.3 The 6.04 billion internet users constitute the absolute maximum theoretical market for any web-based technological deployment.

Smartphone penetration, the primary conduit for digital interaction, closely mirrors broader internet growth. Current data indicates that there are 5.78 billion unique mobile users globally, encompassing 70.1% of the total human population.16 The worldwide unique subscriber figure has increased by 108 million over the past twelve months.16 Furthermore, smartphones now account for roughly 86.9% of all mobile phone handsets currently in use.16 Because the vast majority of consumer generative artificial intelligence interaction occurs via mobile applications or mobile-optimized web browsers, this 5.78 billion figure represents the realistic addressable market for interactive generative artificial intelligence tools under current hardware paradigms.

The data explicitly demonstrates an immovable infrastructural ceiling. Approximately 2.26 billion people remain completely offline in 2026, devoid of any internet access.4 By definition, this offline demographic is categorically excluded from any direct interaction with cloud-based generative artificial intelligence systems. Consequently, any comprehensive analysis of global artificial intelligence adoption must recognize that the so-called “non-user” population is comprised of two distinct geopolitical and economic groups: those who lack the fundamental digital infrastructure to access artificial intelligence, and those who possess internet access but have either chosen not to, or lack the digital literacy to, engage with generative artificial intelligence platforms.

Platform-Level Usage Data

The landscape of generative artificial intelligence is dominated by a tight oligopoly of frontier model developers, supplemented by highly specialized regional ecosystems and medium-specific creative tools. To ascertain a defensible estimate of global human interaction, it is necessary to rigorously deconstruct the active user metrics of the leading platforms, intentionally stripping away registered-user inflation to isolate sustained, habitual usage. The sheer volume of platform interactions highlights a transition from novelty experimentation to daily integration into personal and professional workflows.

The Text and Reasoning Behemoths

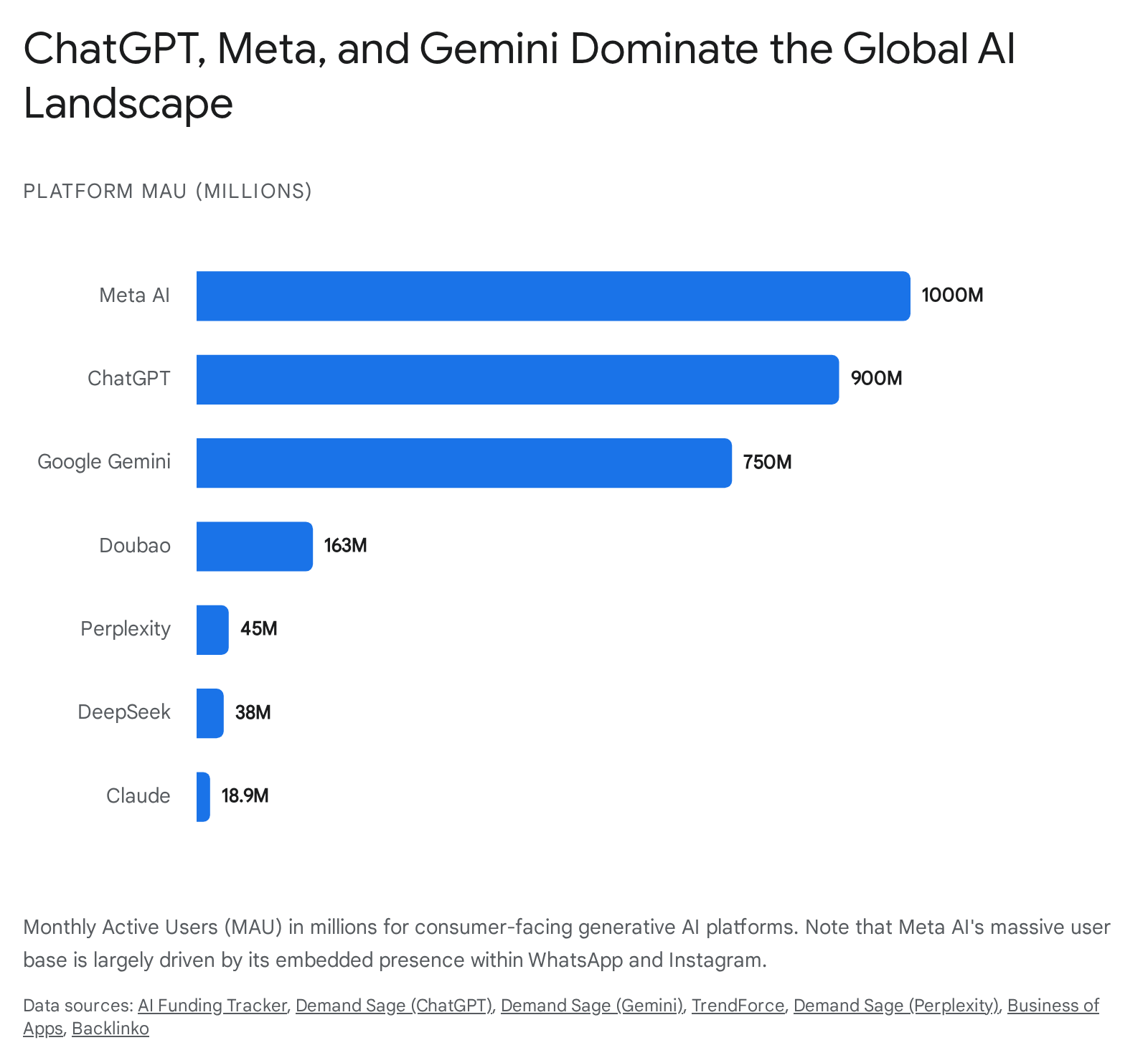

OpenAI’s ChatGPT remains the dominant, culturally ubiquitous gateway for human interaction with generative artificial intelligence. Maintaining a quasi-monopolistic grip on mindshare, ChatGPT holds an estimated 80.49% of the generative artificial intelligence search market share.8 As of early 2026, OpenAI executives disclosed that ChatGPT maintains a staggering 800 million Weekly Active Users, representing a doubling from the 400 million Weekly Active Users reported in February 2025.8 This explosive growth has been significantly bolstered by aggressive international expansion and mobile application rollouts, with India alone contributing an estimated 100 million Weekly Active Users to the platform’s aggregate.8

In terms of raw web traffic, ChatGPT records approximately 5.72 to 5.8 billion monthly visits, processing over 2 billion daily queries and receiving 2.5 billion distinct user prompts each day.8 However, visit volume fundamentally diverges from unique human users. Accounting for high-frequency users who visit the site multiple times per week, the actual unique Monthly Active User base for ChatGPT is estimated to reside just under the 1 billion threshold globally.8 Mobile application downloads further support this vast digital footprint, with over 64 million cumulative application downloads recorded to date.8 The sheer volume of prompts indicates deep, habitual interaction rather than passing conversational experimentation.

Meta has pursued a fundamentally divergent deployment strategy, opting to embed its Meta AI assistant directly into its existing, ubiquitous social and messaging infrastructure rather than relying solely on destination URLs requiring behavioral changes from users. In the first quarter of 2026, Meta announced that Meta AI surpassed 1 billion monthly active users.18 This massive figure is achieved through algorithmic insertion into daily communication workflows. Meta’s internal analytics reveal that WhatsApp serves as the primary gateway, accounting for approximately 630 million Meta AI users, which represents 63% of all artificial intelligence interactions within the corporate ecosystem.19 Instagram contributes roughly 270 million users, primarily engaging with artificial intelligence search, editing tools, and creative assistants, while the older demographic of Facebook yields about 100 million artificial intelligence users.20

By stark contrast, Meta’s standalone Meta AI application, launched to directly compete with ChatGPT, maintains a comparatively modest 10 to 20 million users.20 While Meta boasts an aggregate of 3.48 billion daily active people across its family of applications, the 1 billion artificial intelligence Monthly Active User figure suggests that roughly 30% of its massive user base is actively triggering or utilizing the generative artificial intelligence features embedded within their standard interfaces.18

Google’s Gemini, formerly introduced as Bard, has similarly leveraged its parent company’s pervasive search and mobile operating system ecosystem to rapidly scale its user base. Following its comprehensive rebranding and deep integration into Android devices, Google’s parent company Alphabet reported in February 2026 that Gemini had officially crossed 750 million monthly active users, achieving a net increase of 100 million users from the previous quarter.21 Gemini’s daily active user count is estimated at roughly 35 million, suggesting a Daily Active User to Monthly Active User ratio of approximately 4.6% to 7.8%.23 This metric indicates that while hundreds of millions of people interact with Gemini monthly—often prompted by seamless integrations into Google Workspace tools like Docs and Gmail, or native Android operating system prompts—the platform is still cultivating the habitual, high-frequency daily usage seen in traditional search behaviors.23 Furthermore, Gemini technology actively powers Google’s “AI Overviews,” which reach an estimated 2 billion users monthly; however, this specific implementation is classified as invisible artificial intelligence or search ranking for the purposes of this report’s strict interactivity definitions, and is therefore excluded from direct usage counts.21

Challengers, Regional Leaders, and Technical Specialists

The geographical localization of generative artificial intelligence has resulted in the creation of highly siloed regional ecosystems, particularly within the regulatory boundaries of China. ByteDance’s Doubao has emerged as the clear domestic leader in this theater. Operating with remarkably minimal marketing expenditure and driven by massive organic traffic distribution from its sister application Douyin (the Chinese domestic iteration of TikTok), Doubao reached 163 million Monthly Active Users and 155 million Weekly Active Users by the conclusion of 2025.26 Notably, Doubao’s daily active user count surpassed 100 million, indicating a highly engaged user base that processes over 50 trillion tokens daily across text, image, and video generation requests.26

Concurrently, DeepSeek has catalyzed significant disruption within the broader global market. Releasing highly capable, open-weight reasoning models at a fraction of Western computational and training costs, DeepSeek achieved an average of 38 million Monthly Active Users by early 2026.29 While 30.7% of its user base remains concentrated natively in China, DeepSeek has established a remarkably substantial global footprint, achieving strong adoption rates in India (13.6%), Indonesia (6.9%), and the United States (4.3%).30 The DeepSeek mobile application experienced an explosive growth trajectory, registering nearly 20 million downloads in February 2025 alone following the highly publicized release of its R1 model, positioning it as a formidable competitor to established Western incumbents.31

Anthropic’s Claude and Perplexity AI represent the premium, productivity-focused tier of the market, prioritizing accuracy, extended context windows, and search-grounded reasoning over pure conversational volume. Claude reported approximately 18.9 million to 19 million Monthly Active Users globally, with 2.9 million users accessing its dedicated mobile application.33 Despite possessing a markedly smaller consumer user base compared to OpenAI, Anthropic brings in substantial capital—projected at over $3 billion in annualized revenue—driven predominantly by heavy enterprise integration and API usage.34 Research indicates that Claude’s usage is highly correlated with national Gross Domestic Product; users in high-income nations predominantly utilize the tool for advanced personal productivity and high-skill corporate tasks, whereas users in lower-GDP nations skew heavily toward utilizing it for educational and coursework assistance.35

Perplexity AI, operating explicitly as an artificial intelligence-native search engine rather than a general-purpose chatbot, reached 45 million Monthly Active Users and 170 million monthly web visitors by early 2026.36 Processing roughly 780 million monthly queries, Perplexity boasts a highly professional, workflow-integrated user base. Demographic data indicates that 55% of queries are for personal use, 30% for professional workflows—such as advanced computer programming, email management, and financial data editing—and 15% for complex educational research.37

The Evolution of AI Video and Image Generation

The multimedia generation sector has profoundly matured, transitioning from rudimentary static image creation to high-fidelity, physically consistent video generation. Midjourney remains the predominant, undisputed image generation platform, boasting roughly 21 million registered users heavily concentrated on its Discord server integration.11 The platform’s daily active users consistently fluctuate between 1.2 million and 2.5 million, with users collectively engaging in up to 40 complex image generation tasks per second globally during peak periods.10

In the highly resource-intensive video generation sphere, competition is fierce but aggregate usage remains severely constrained by high computational costs, restrictive commercial licensing, and lengthy rendering times. OpenAI’s Sora application experienced a highly volatile trajectory; after peaking in late 2024, the application saw its mobile downloads drop precipitously by 45% to just 1.2 million in January 2026 amid rising competition, stringent copyright restrictions, and consumer frustration over generation limits.41 Challengers such as Kuaishou’s Kling AI and Luma’s Dream Machine have subsequently captured significant market share among creative professionals, advertising agencies, and filmmakers due to substantially faster rendering speeds, superior physical consistency, and highly accessible tiered pricing models.42 However, despite the intense industry focus, the total unique user numbers for these advanced video generation platforms remain confined to the low millions, lacking the mass consumer penetration seen in text-based conversational agents.

Paid Subscription Estimates

Estimating the total number of individuals financially contributing to the generative artificial intelligence ecosystem requires rigorously dissecting the market into distinct consumer subscriptions and enterprise licenses. While free tiers drive the massive adoption metrics previously discussed, the conversion to paid tiers reveals the actual perceived economic and productivity value of these tools to the end user.

Consumer willingness to pay subscription fees ranging from $10 to $20 per month for premium large language model access—such as ChatGPT Plus, Claude Pro, and Perplexity Pro—is robust, yet it represents a minute fraction of total active users. OpenAI decisively leads the consumer subscription market, with an estimated 10 million users globally paying for premium access to the ChatGPT ecosystem.8 This translates to roughly $2.4 billion in annual recurring revenue derived exclusively from consumer subscriptions. Midjourney, operating entirely on a subscription model without a permanent free generation tier, maintains approximately 2 million actively paying users.45 With subscription plans scaling from $10 to $120 monthly based on GPU allocation times, Midjourney generates an estimated $500 million in annual revenue.39 Factoring in the smaller subscriber bases for Perplexity Pro, Claude Pro, and mobile-native applications such as Nova and Character AI premium tiers, the total global pool of consumers paying out-of-pocket for generative artificial intelligence subscriptions is bounded between 16 million and 25 million individuals.

The enterprise sector represents a far more lucrative and scalable growth vector, characterized by top-down corporate procurement of artificial intelligence “seats” or “copilots” deeply integrated into existing legacy software suites. Microsoft has aggressively and successfully monetized its existing commercial user base through this mechanism. In its Q2 FY26 earnings call, Microsoft revealed it had reached 15 million paid Microsoft 365 Copilot seats, demonstrating an astonishing 160% year-over-year growth trajectory.9 At $30 per user per month, this represents massive revenue generation, though it must be carefully contextualized: the 15 million paid seats represent only 3.3% of Microsoft’s massive 450 million overall commercial Microsoft 365 user base, indicating both a sluggish initial enterprise rollout and vast uncaptured market potential.9

While Alphabet does not explicitly bifurcate consumer versus enterprise paid seats for its Gemini Advanced offerings, corporate disclosures note that over 120,000 distinct enterprises—including 95% of the top 20 global software-as-a-service companies—are currently utilizing Gemini within their operational workflows.21 Similarly, Anthropic has shifted focus toward B2B integration, with over 50% of its $3.3 billion projected revenue deriving directly from enterprise and API usage.34

Synthesizing these disparate corporate data points, the global total of paid generative artificial intelligence users—encompassing individual consumers, freelance creatives, and corporate employees utilizing licensed digital seats—is estimated to be securely positioned between 35 million and 60 million individuals. This calculation indicates that roughly 3% to 5% of the total monthly active generative artificial intelligence user base interacts with a premium, directly monetized version of the technology.

AI Coding Assistant Adoption

The discipline of software development has experienced the most profound paradigm shift of any professional sector due to the advent of generative artificial intelligence. Artificial intelligence coding assistants, which autonomously autocomplete complex code strings, debug deep architectural errors, and explain legacy codebases, have rapidly evolved from experimental novelties to standard, indispensable industry tooling.

To accurately measure penetration rates within this sector, a definitive baseline population must first be established. According to Statista and Organization for Economic Co-operation and Development workforce benchmarks, the global software developer population reached precisely 28.7 million individuals by the end of 2025.14 This highly specialized workforce is geographically distributed, with major operational hubs located in China, boasting 7 million developers, followed by the United States with 2.9 million, and India functioning as a major outsourcing hub with 2.6 million developers.14

Generative artificial intelligence adoption within this specific professional cohort is exceptionally high, eclipsing adoption rates in any other industry. Stack Overflow’s definitive 2025 Developer Survey, which compiled insights from over 49,000 developers globally, revealed that a remarkable 80% of software developers are now actively using artificial intelligence tools within their daily operational workflows.15 Applying this 80% penetration rate to the 28.7 million global developer population yields an estimated 22.9 million individual developers utilizing artificial intelligence coding assistants worldwide.

GitHub Copilot, heavily backed by Microsoft infrastructure, maintains a dominant market share of approximately 42% within the artificial intelligence coding tools sector.13 In July 2025, GitHub announced that Copilot had officially reached 20 million cumulative users.13 However, this cumulative metric encompasses free trials, educational student accounts, and inactive historical registrations. More accurately reflecting sustained, high-value commercial usage, GitHub Copilot reported 1.3 million actively paid subscribers in Q1 2025, with institutional adoption occurring in 90% of Fortune 100 companies.13

Despite near-universal adoption rates across the industry, the daily interaction is increasingly fraught with operational friction. As usage has scaled to handle more complex architectural challenges, developer confidence in the technology has inversely declined. Trust in the fundamental accuracy of artificial intelligence-generated code fell precipitously from 40% in early adopter cohorts to just 29% in the 2025 survey period.15 Furthermore, 66% of developers report spending significantly increased time fixing “almost-right” artificial intelligence-generated code, citing complex debugging as their primary frustration with the technology.15 This indicates that while 23 million developers routinely interact with generative artificial intelligence, the fundamental nature of that interaction has shifted violently from unquestioning reliance to highly skeptical, time-consuming verification.

Non-User Population Estimate

Understanding the true societal reach of generative artificial intelligence inherently requires estimating the vast population that does not interact with it. This necessitates calculating the unique human user base mathematically and subtracting it from the established global population.

Summing the unadjusted Monthly Active Users of the top global platforms—including Meta AI’s 1 billion, ChatGPT’s nearly 1 billion, Gemini’s 750 million, and Doubao’s 163 million—yields an aggregate figure well exceeding 2.9 billion interactions. However, utilizing this figure is a gross misrepresentation of unique human users due to the pervasive phenomenon of extreme multi-homing. A single professional software engineer might habitually use GitHub Copilot for backend coding, ChatGPT for drafting corporate communications, Perplexity for deep technical research, and Midjourney for generating presentation aesthetics. That single human being represents four distinct Monthly Active Users recorded across four different corporate ledgers.

To mathematically account for this severe overlap, leading analytics firms and institutional researchers utilize highly deduplicated telemetry and survey panels. Comprehensive analysis conducted by Kepios and We Are Social concludes with high confidence that “well over 1 billion people now use standalone AI tools each month”.5 Corroborating this foundational estimate, Microsoft’s Global AI Adoption Report, which relies on anonymized global operating system telemetry, determined that 16.3% of the world’s working-age population utilized generative artificial intelligence tools in the second half of 2025.6 By applying these rigorously deduplicated penetration rates against the global population, this report establishes a highly defensible mid-point estimate of 1.2 billion unique human users interacting with generative artificial intelligence globally on a monthly basis.

Utilizing the established demographic baselines, the non-user calculation is straightforward. Subtracting the 1.2 billion unique generative artificial intelligence users from the global population of 8.3 billion results in a total non-user population of 7.1 billion individuals. Therefore, approximately 7.1 billion human beings have not interacted with generative artificial intelligence in any sustained, identifiable manner as of early 2026.

This non-user population must be further segmented to understand the nature of the divide. As previously noted in the baseline context, 2.26 billion people are entirely offline and digitally disenfranchised.4 Subtracting the entirely offline population from the 7.1 billion total non-users reveals that roughly 4.84 billion people possess baseline internet access but choose not to, or fundamentally do not know how to, utilize generative artificial intelligence tools. Pew Research explicitly corroborates this behavioral gap; while global awareness of the technology is steadily rising, 44% of Americans explicitly state they do not regularly use artificial intelligence, and in developing nations like Kenya and India, vast majorities report having heard “nothing at all” about the technology’s existence or utility.48

Geographic and Income Distribution

Generative artificial intelligence adoption is definitively not a uniform global phenomenon; rather, it is characterized by stark regional clustering and a profound, undeniable correlation with national income levels and pre-existing digital infrastructure.

Data derived from the Microsoft AI Economy Institute reveals a rapidly widening digital divide separating global economic spheres. In the second half of 2025, generative artificial intelligence diffusion in the Global North reached a robust 24.7% of the working-age population.6 Conversely, systemic adoption in the Global South stood at an anemic 14.1%.6 More critically concerning than the baseline disparity is the rate of systemic growth; adoption in the Global North grew almost twice as fast—increasing by 1.8 percentage points—compared to the Global South, which increased by only 1.0 percentage points over a concurrent six-month period, stretching the global adoption gap to an unprecedented 10.6 percentage points.6

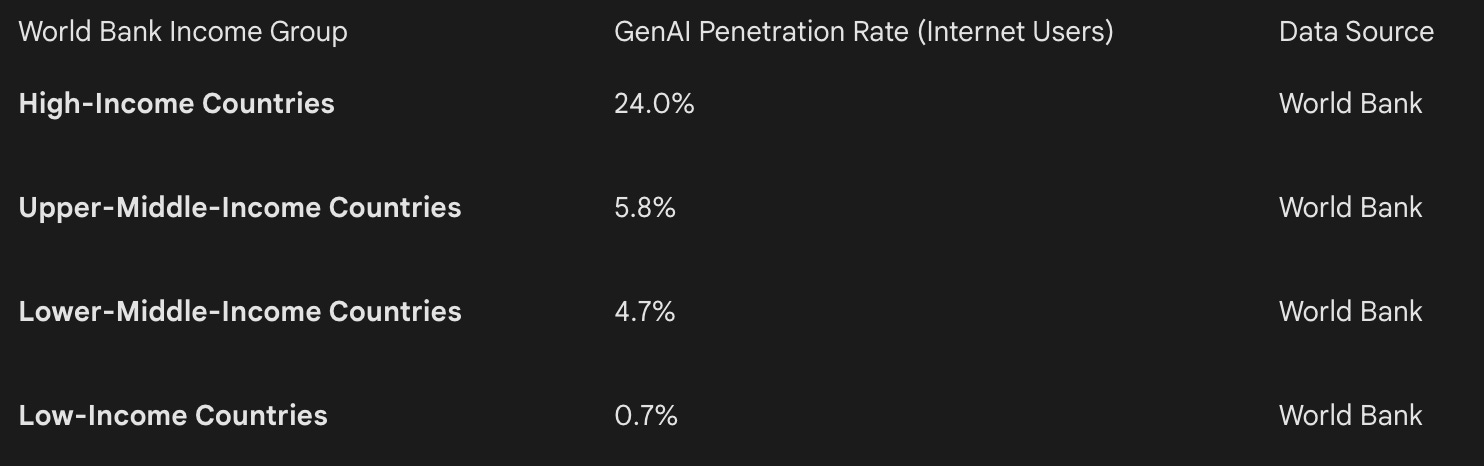

A comprehensive 2025 World Bank analysis utilizing high-frequency website traffic data provides an even sharper delineation of this deep inequality based strictly on Gross Domestic Product per capita classifications.

The data contained within this table unequivocally confirms that national wealth remains the single strongest predictor of generative artificial intelligence adoption growth. Users located in high-income economies aggressively leverage these tools to drive top-line corporate growth and individual enterprise efficiency, whereas meaningful adoption in lower-income regions is severely hampered by a lack of localized language models, lower aggregate digital literacy, and severe hardware and broadband constraints.51

Despite these broader regional trends, certain nations dramatically outperform the global average due to highly aggressive national artificial intelligence skilling initiatives and robust state-sponsored digital infrastructure. The United Arab Emirates leads the global community with a staggering 64.0% artificial intelligence usage rate among its working-age population.6 Singapore follows closely behind with an adoption rate of 60.9%.6 In Europe and Oceania, nations such as Norway at 46.4%, Ireland at 44.6%, France at 44.0%, and New Zealand at 40.5% demonstrate highly robust, mature societal adoption.6 Surprisingly, despite being the undisputed corporate epicenter of foundational model development—hosting OpenAI, Google, Anthropic, and Meta—the United States ranks 24th globally in proportional population adoption, maintaining a 28.3% usage rate that heavily trails smaller, more highly digitized economies.6

Analytical Framework and Data Quality Review

The nascent, hyper-competitive nature of the generative artificial intelligence industry inherently results in significant variances in corporate data reporting and measurement methodologies. Any comprehensive estimate attempting to quantify human interaction must rigorously address the systemic biases, regional blind spots, and methodological inflation inherent in the available source material.

A primary vulnerability in assessing artificial intelligence adoption lies in the frequent corporate conflation of “registered accounts” with sustained “active users.” Generative artificial intelligence platforms experienced massive, viral consumer testing phases throughout 2023 and 2024, resulting in historically unprecedented initial account creation metrics. However, long-term retention remains a distinct operational challenge. Midjourney, as an illustrative example, proudly boasts 21 million registered users on its Discord server integration, yet its daily active user base consistently fluctuates between just 1.2 million and 2.5 million users.10 Similarly, while ChatGPT recorded an immense 5.72 billion monthly web visits, calculating actual unique human users requires a dramatic mathematical downward adjustment to properly account for individuals executing dozens of distinct queries within a single web session.8 Corporate disclosures frequently highlight cumulative historical totals, such as GitHub Copilot’s 20 million users, rather than actively paying seats, which sit at a much lower 1.3 million, requiring careful distillation to avoid projecting false precision.13

Furthermore, measuring true “interaction” becomes highly subjective when artificial intelligence is embedded invisibly into existing, ubiquitous products. Meta’s headline claim of 1 billion Monthly Active Users for Meta AI relies intensely on its algorithmic integration into WhatsApp’s search and chat functionalities.18 Because the artificial intelligence interface is triggered within a pre-existing social communication habit, distinguishing intentional artificial intelligence utilization from accidental or passive engagement is methodologically difficult. While this report adheres strictly to definitions requiring active, prompted interaction, embedded interfaces inherently inflate perceived adoption rates when directly compared to standalone destination platforms like Claude or Perplexity, where the user must exhibit explicit intent to navigate to the service.

Survey-based estimates also inherently suffer from well-documented self-reporting bias. In the Stack Overflow developer survey, participants self-select to participate, potentially skewing the highly touted 80% adoption figure toward more technologically progressive developers, while subsequently undercounting legacy enterprise coders operating in highly restricted environments.15 Similarly, global consumer surveys face severe regional blind spots. DeepSeek’s rapid, explosive ascent in China and the broader global open-source community distinctly demonstrates that Western-centric analytics tracking—which primarily monitors the usage of OpenAI, Google, and Anthropic—often vastly underestimates actual adoption occurring in Asia, Russia, and Africa.30

Finally, the term “usage” currently lacks meaningful industry standardization. A casual user who generates one novelty image a month on Midjourney is weighed equally in standard Monthly Active User statistics against a professional software developer who spends six hours a day pair-programming with an enterprise Copilot. Consequently, while the synthesis of available data leads this report to conclude that 1.2 billion humans interact with generative artificial intelligence, the actual depth, frequency, and economic value of that interaction remain highly uneven, heavily concentrated among a much smaller, elite cohort of daily power users and paying enterprise subscribers.

Works cited

World population - Wikipedia, accessed February 22, 2026, https://en.wikipedia.org/wiki/World_population

Digital 2026: global population trends - DataReportal, accessed February 22, 2026, https://datareportal.com/reports/digital-2026-global-population-trends

Digital 2026: internet users pass the 6 billion mark - DataReportal, accessed February 22, 2026, https://datareportal.com/reports/digital-2026-six-billion-internet-users

Statistics - ITU, accessed February 22, 2026, https://www.itu.int/en/ITU-D/Statistics/pages/stat/default.aspx

Digital 2026: Global Overview Report - DataReportal, accessed February 22, 2026, https://datareportal.com/reports/digital-2026-global-overview-report

Global AI Adoption in 2025 - A Widening Digital Divide - Microsoft, accessed February 22, 2026, https://www.microsoft.com/en-us/research/wp-content/uploads/2026/01/Microsoft-AI-Diffusion-Report-2025-H2.pdf

Digital 2026: more than 1 billion people use AI - DataReportal, accessed February 22, 2026, https://datareportal.com/reports/digital-2026-one-billion-people-using-ai

ChatGPT Users Statistics (FEB 2026) - Global Growth & Usage - DemandSage, accessed February 22, 2026, https://www.demandsage.com/chatgpt-statistics/

Microsoft’s Copilot User Growth and Market Potential, accessed February 22, 2026, https://intellectia.ai/news/stock/microsofts-copilot-user-growth-and-market-potential

Midjourney Statistics - Quantumrun Foresight, accessed February 22, 2026, https://www.quantumrun.com/consulting/midjourney-statistics/

Midjourney Statistics 2026 (Active Users & Revenue) - DemandSage, accessed February 22, 2026, https://www.demandsage.com/midjourney-statistics/

Microsoft Reports 15M Paid Copilot Users 02/10/2026, accessed February 22, 2026, https://www.mediapost.com/publications/article/412679/microsoft-reports-15m-paid-copilot-users.html?edition=141530

GitHub Copilot Statistics 2026 - Quantumrun Foresight, accessed February 22, 2026, https://www.quantumrun.com/consulting/github-copilot-statistics/

Software Development Statistics: 2026 Market Size, Developer Trends & Technology Adoption, accessed February 22, 2026, https://keyholesoftware.com/software-development-statistics-2026-market-size-developer-trends-technology-adoption/

Developers remain willing but reluctant to use AI: The 2025 Developer Survey results are here - The Stack Overflow Blog, accessed February 22, 2026, https://stackoverflow.blog/2025/12/29/developers-remain-willing-but-reluctant-to-use-ai-the-2025-developer-survey-results-are-here/

Digital 2026 Global Overview Report - We Are Social UK, accessed February 22, 2026, https://wearesocial.com/uk/blog/2025/10/digital-2026-global-overview-report/

Number of ChatGPT Users (January 2026) - Exploding Topics, accessed February 22, 2026, https://explodingtopics.com/blog/chatgpt-users

Meta AI Users Statistics (2026) – Weekly & Daily Active Users - DemandSage, accessed February 22, 2026, https://www.demandsage.com/meta-ai-users/

Make-A-Video Statistics 2026 - Quantumrun Foresight, accessed February 22, 2026, https://www.quantumrun.com/consulting/make-a-video-statistics/

Meta AI News 2026: New Models, Nvidia Deal & 1 Billion User Milestone, accessed February 22, 2026, https://aifundingtracker.com/meta-ai-news/

accessed February 22, 2026, https://www.demandsage.com/google-gemini-statistics/

Gemini User Base Surpasses 750 Million: Google’s Strong Financial Report Keeps Close to ChatGPT - Why AIBase?, accessed February 22, 2026, https://news.aibase.com/news/25278

50+ Google Gemini AI Statistics for 2026 - Sociallyin, accessed February 22, 2026, https://sociallyin.com/gemini-ai-statistics/

Google Gemini Revenue and Usage Statistics (2026) - Business of Apps, accessed February 22, 2026, https://www.businessofapps.com/data/google-gemini-statistics/

Google Gemini Stats Feb 2026 – Market Share, Users and More. - fatjoe., accessed February 22, 2026, https://fatjoe.com/blog/google-gemini-stats/

ByteDance’s Doubao reaches 100M DAU with minimal marketing spend - TechNode, accessed February 22, 2026, https://technode.com/2025/12/25/bytedances-doubao-reaches-100m-dau-with-minimal-marketing-spend/

China’s ByteDance releases Doubao 2.0 AI model for ‘agent era’ | 1330 & 101.5 WHBL, accessed February 22, 2026, https://whbl.com/2026/02/14/chinas-bytedance-releases-doubao-2-0-ai-chatbot/

[News] ByteDance, Alibaba, DeepSeek Reportedly Ready February Model Launches, Fueling China’s AI Race - TrendForce, accessed February 22, 2026, https://www.trendforce.com/news/2026/01/30/news-bytedance-alibaba-deepseek-reportedly-ready-february-model-launches-fueling-chinas-ai-race/

DeepSeek Revenue and Usage Statistics (2026) - Business of Apps, accessed February 22, 2026, https://www.businessofapps.com/data/deepseek-statistics/

60 Latest DeepSeek Statistics (2026) - Thunderbit, accessed February 22, 2026, https://thunderbit.com/blog/deepseek-ai-statistics

DeepSeek AI Statistics 2026 [Revenue & Users] - DemandSage, accessed February 22, 2026, https://www.demandsage.com/deepseek-statistics/

DeepSeek AI Usage Stats for 2026 - Backlinko, accessed February 22, 2026, https://backlinko.com/deepseek-stats

Claude Statistics 2026: How Many People Use Claude? - Backlinko, accessed February 22, 2026, https://backlinko.com/claude-users

Claude Revenue and Usage Statistics (2026) - Business of Apps, accessed February 22, 2026, https://www.businessofapps.com/data/claude-statistics/

Anthropic Economic Index report: Economic primitives, accessed February 22, 2026, https://www.anthropic.com/research/anthropic-economic-index-january-2026-report

Perplexity AI Statistics 2026 – Active Users & Revenue - DemandSage, accessed February 22, 2026, https://www.demandsage.com/perplexity-ai-statistics/

Perplexity AI Stats Feb 2026: Uses, Users, Market Share, and More. - fatjoe., accessed February 22, 2026, https://fatjoe.com/blog/perplexity-ai-stats/

Perplexity AI User Statistics 2026 (Updated this February) - clickvision, accessed February 22, 2026, https://click-vision.com/perplexity-ai-user-statistics

Midjourney Statistics - About Chromebooks, accessed February 22, 2026, https://www.aboutchromebooks.com/midjourney-statistics/

54+ Unique Midjourney Statistics - Users, Growth, Revenue - BrandWell, accessed February 22, 2026, https://brandwell.ai/blog/midjourney-statistics/

OpenAI’s Sora App Hits Turbulence After Meteoric Rise - The Tech Buzz, accessed February 22, 2026, https://www.techbuzz.ai/articles/openai-s-sora-app-hits-turbulence-after-meteoric-rise

Sora vs Kling AI 2026: The Data-Backed Truth - AI Efficiency Hub, accessed February 22, 2026, https://ai-coding-flow.com/blog/sora-vs-kling-ai-2026/

Luma Dream Machine Pricing Breakdown (2026): Cost, Tiers & Hidden Fees, accessed February 22, 2026, https://www.photonpay.com/hk/blog/article/luma-dream-machine-pricing?lang=en

Runway vs Pika vs Luma AI – A Complete Guide for Marketing Leaders in 2026, accessed February 22, 2026, https://genesysgrowth.com/blog/runway-vs-pika-vs-luma-ai

Midjourney in 2026: Usage, Revenue, Valuation & Growth Statistics - Fueler, accessed February 22, 2026, https://fueler.io/blog/midjourney-usage-revenue-valuation-growth-statistics

Microsoft spends billions on AI, converts just 3.3% of Copilot Chat users - The Register, accessed February 22, 2026, https://www.theregister.com/2026/02/02/microsoft_ai_spend_copilot/

Microsoft Quarterly Report Details Big Customer Wins in Agents, Copilots, and Healthcare, accessed February 22, 2026, https://cloudwars.com/ai/microsoft-quarterly-report-details-big-customer-wins-in-agents-copilots-and-healthcare/

131 AI Statistics and Trends for 2026 | National University, accessed February 22, 2026, https://www.nu.edu/blog/ai-statistics-trends/

How People Around the World View AI - Pew Research Center, accessed February 22, 2026, https://www.pewresearch.org/global/2025/10/15/how-people-around-the-world-view-ai/

Mapped: AI Adoption Rates by Country - Visual Capitalist, accessed February 22, 2026, https://www.visualcapitalist.com/ai-adoption-rates-by-country/

Publication: Who on Earth Is Using Generative AI? Global Trends and Shifts in 2025 - Open Knowledge Repository - World Bank, accessed February 22, 2026, https://openknowledge.worldbank.org/entities/publication/f4eea48b-41cd-4242-87ad-82dfa0dc85f2

Publication: Who on Earth Is Using Generative AI - Open Knowledge Repository, accessed February 22, 2026, https://openknowledge.worldbank.org/entities/publication/5a876bd0-f85a-479b-ae32-cf0b7f33792f

Global AI Adoption in 2025 – AI Economy Institute - Microsoft, accessed February 22, 2026, https://www.microsoft.com/en-us/corporate-responsibility/topics/ai-economy-institute/reports/global-ai-adoption-2025/